![]()

17 Mar, 2021

What is Speculative Transactions under Income Tax Act" />

What is Speculative Transactions under Income Tax Act" />

As per Section 43 (5) of the Income Tax Act, Speculative transaction is a transaction where a contract for the purchase or the sale of any commodity, including stocks and shares is periodically or is ultimately settled otherwise than by the actual delivery or transfer of the commodity or scrip. In this article, we shall discuss Speculative transactions in brief.

In case of intra-day trading in shares, there is no actual delivery since the shares enter to and exit from the trading account on the same date, and it doesn’t enter the DEMAT account at all. Intra-day trading refers to the trading of shares within the same day. Usually, the delivery is not taken in the case of intra-day trading. Therefore they are called Speculative Transactions.

In the above mentioned definition of Speculative transaction, the important thing to note is “periodically or is ultimately settled otherwise than by actual delivery.” This means physical delivery is not made.

Section 28, explanation 2, states that business of the assessee should be deemed as distinct and separate from any other business where such assessee carries on speculative business.

The above mentioned point is critical as Section 73 states that losses in the speculation business, unlike any other business, can’t be set off against the income of any business other than a speculation business.

A loss in speculation business that is carried forward to a succeeding year can only be set off against the profit and gains of any speculative business in the subsequent year. No loss can be carried forward under this section to beyond four assessment years period immediately succeeding an assessment year for which the loss was computed.

READ Key Implications of the Taxation Bill 2020 on ITR FilingIn case any portion of the business of the company consists in the purchase and sale of the shares of other companies, the company will be deemed to be carrying on a speculation business to an extent to which the business has sale and purchase of such shares.

The provision mentioned above doesn’t apply to the companies as mentioned below:

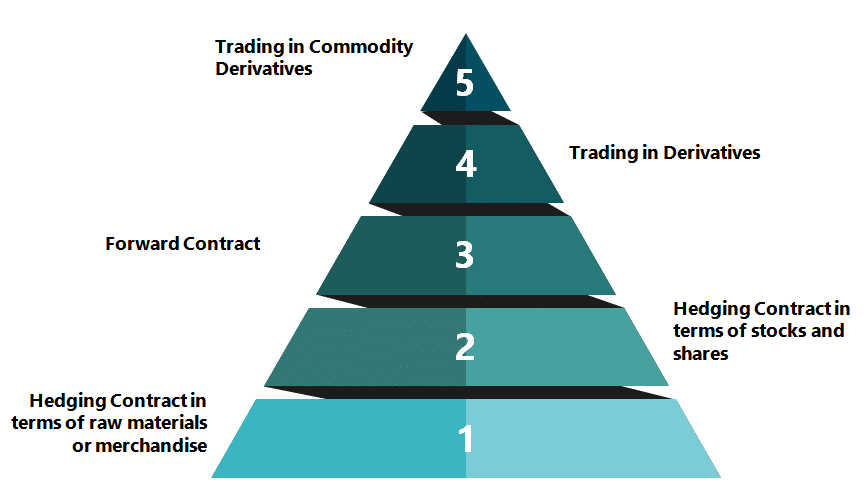

The following shall not be deemed as Speculative transactions:

Few types of these transactions and how they are conducted in stock exchanges are mentioned below:

It refers to the right to buy or sell a security within a prescribed time at a prescribed price. The right to purchase securities is called the call option, and right to sell securities is called the put option.

In this shares are bought from money borrowed from the brokers. The client opens an account with the broker. He then deposits cash or securities into the account and agrees to maintain the margin at a level. When the broker buys securities, the clients’ account is debited with the amount of such securities.

It refers to benefiting from the difference in the price of a security prevailing in two exchanges. The arbitrager buys the security at which it’s cheaper and sells it in the market where it is costlier.

This refers to a transaction where a speculator sells a security from one broker and buys the same security through another broker but at a higher price.

It means a situation where an individual or a group acquires a significant portion of company’s shares.

The transfer deed has details of only the seller. The buyer details are not mentioned. It is now banned as it encourages tax evasion.

In case of Speculative transactions, there is no receiving or giving delivery of shares/goods or stocks. The contract is settled by paying the differences in selling and purchase price, which can be positive or negative.